Thursday, 9 July 2026

The procurement of Totapuri Mangoes will be carried out under the MIS, with the Market Intervention Price fixed at Rs. 1,545.41 per quintal while Copra procurement will be undertaken at…

Comprehensive documentation requirements aim to strengthen food safety while raising the regulatory burden on global exporters South Africa has reinforced its import certification regime for food and agricultural products by…

Recently APEDA facilitated commercial export of 2 metric tonnes (MT) of Amrapali mangoes from Jharkhand to Dubai. The Agricultural and Processed Food Products Export Development Authority (APEDA), under the Ministry…

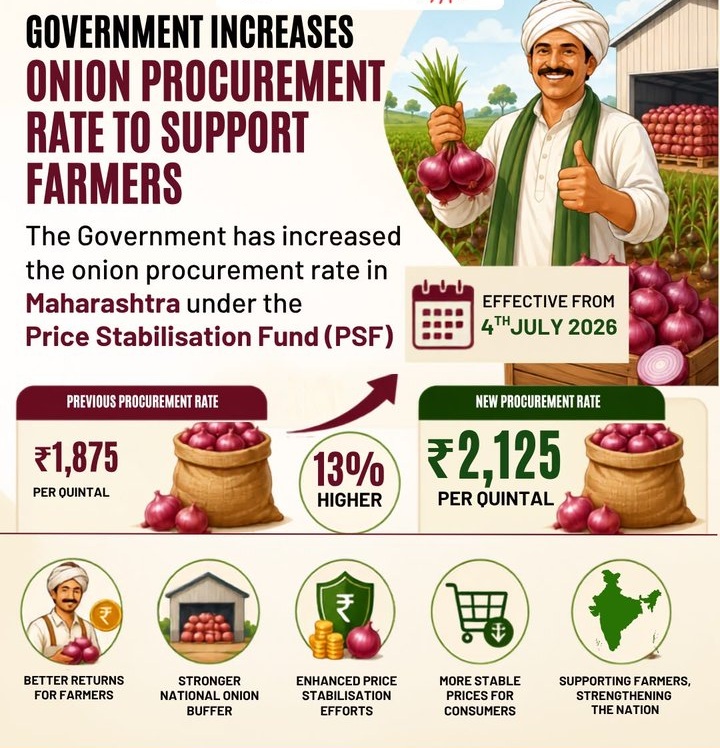

The revised procurement price will ensure better returns for onion farmers while supporting buffer procurement efforts. The Government has increased the procurement price of onions for the Price Stabilisation Buffer…

The real outcome of edge AI isn’t the engineering — it’s what it unlocks for the businesses that serve farmers. Farmers benefit in the end, sure, but the ones actually…

World Bank-supported initiative aims to accelerate climate-resilient agriculture through technology, innovation and farmer-centric entrepreneurship In a major push to strengthen India’s agri-tech innovation ecosystem, the Government of Kerala has launched…

The innovative reaction vessel has been designed for a low cost, smart, robust reaction system enabling synthesis of chemical and green nanoparticles and advanced formulations like nano-fertilizers, nano-minerals, nano-pesticides etc.…

New digital tool combines soil, climate and landscape data to improve yields, strengthen resilience and support smarter farming Farmers, extension workers and governments now have a powerful new tool to…

Dr. Daya Pandey discusses why India must move beyond landfill-centric waste management and embrace circular bioeconomy solutions to strengthen energy security, public health and environmental sustainability In this insightful Agrospectrum…

Collaboration to develop and commercialize new formulations and mixtures Crystal Crop Protection Limited, a premier research-driven agriculture input company, and Corteva, a global pure-play agriculture company combining industry-leading innovation, high-touch…

Strengthening its rice crop protection portfolio, UPL’s Ricebeaux, a early post rice herbicide developed over 10 years of research and validated through multi-locational trials offers broad-spectrum control of grasses, sedges…

One vision calls for 45 million tonnes of mineral fertilizers by 2050. Another believes smarter agriculture can achieve the same harvest with far fewer inputs For decades, India’s agricultural strategy…

Under the agreement, UPL SAS will deploy a dedicated Program Officer to lead field-level implementation and farmer engagement activities UPL Sustainable Agri Solutions Limited (UPL SAS), a leading provider of…

As geopolitical shocks, climate stress and subsidy pressures intensify, experts argue that India’s food security will depend less on applying more fertiliser and more on using every nutrient and every…