Thursday, 2 July 2026

As geopolitical shocks, climate stress and subsidy pressures intensify, experts argue that India’s food security will depend less on applying more fertiliser and more on using every nutrient and every drop of water more efficiently

India’s agricultural future is increasingly being shaped by forces far beyond its farms. Wars in distant geographies, shipping disruptions in strategic waterways, volatile energy markets and erratic climate events are now directly influencing what Indian farmers pay for fertilisers, how industries procure raw materials and how much the government spends on subsidies. The old assumption that global disruptions are temporary has been shattered. According to industry experts, these risks are no longer episodic disturbances but structural realities that will define the future of Indian agriculture.

Mahesh Damodare, Director of Dhanashree Crop Solutions Pvt. Ltd., argues that Indian agriculture has entered a new era where fertiliser security has become inseparable from food security, economic stability and climate resilience. He identifies three major risks confronting Indian agriculture—geopolitical risk arising from conflicts in regions such as the Middle East and the Russia-Ukraine theatre, economic risks in the form of ballooning subsidies and currency volatility, and climate risks driven by El Niño events and growing water scarcity. “These risks are no longer temporary. They are becoming structural,” he says, warning that the country can no longer view fertiliser availability as merely an agricultural issue.

India’s vulnerability begins with its dependence on imported energy. Around 40-43 per cent of India’s liquefied natural gas imports come from Qatar, while the United States contributes 10-12 per cent, the UAE around 9-10 per cent, and countries such as Nigeria, Angola and Oman contribute another 6-7 per cent each. This dependence exposes India to extreme price fluctuations. Global LNG prices averaged around $ 12-13 per MMBtu in 2025, softened to approximately $ 10-11 per MMBtu in January 2026, only to surge dramatically to $ 20-25 per MMBtu in March 2026 before moderating to around $ 18-19 per MMBtu in June. Since natural gas is the primary feedstock for urea production, these movements directly influence fertiliser costs and subsidy requirements.

India’s dependence on imported fertilisers further magnifies the risks. In 2024-25, the country imported 56.47 lakh metric tonnes of urea and 35.41 lakh metric tonnes of DAP. The concentration of suppliers is particularly striking. Oman alone supplied 26.13 lakh metric tonnes of urea, accounting for 46 per cent of imports, followed by Russia with 9.23 lakh metric tonnes or 16 per cent. Saudi Arabia contributed 5.38 lakh metric tonnes, Qatar 3.70 lakh metric tonnes, the UAE 3.39 lakh metric tonnes, Nigeria 2.83 lakh metric tonnes and China nearly one lakh metric tonnes. Together, Oman and Russia account for 62 per cent of India’s urea imports.

The dependence is even sharper in DAP. Russia supplied 18 lakh metric tonnes or 51 per cent of India’s DAP imports, while Canada accounted for another 8.83 lakh metric tonnes or 25 per cent. Jordan, Israel and Turkmenistan contributed 9 per cent, 8 per cent and 8 per cent respectively. Consequently, Russia and Canada together account for an overwhelming 76 per cent of India’s DAP imports, creating significant supply vulnerabilities.

The Russia-Ukraine war exposed these vulnerabilities with unprecedented clarity. Before the conflict, urea prices stood at around $ 263 per tonne. They surged to $ 661 per tonne during the peak of the crisis, representing an increase of nearly 150 per cent. Prices subsequently declined to around $ 370 per tonne in 2023-24 and stabilised between $ 330 and $ 360 per tonne during 2024-25, only to spike again to nearly $ 800 per tonne by June 2026. The latest increase represents a rise of 115-140 per cent over the previous stable phase.

DAP prices witnessed a similarly dramatic trajectory. Prices increased from $ 369 per tonne before the war to between $ 741 and $ 805 per tonne during the crisis, a rise of nearly 120-130 per cent. Although prices later moderated to around $ 556 per tonne and stabilised in the $ 540-580 per tonne range during 2024-25, they surged once again to $ 792 per tonne by May 2026, representing another increase of 35-47 per cent.

The war produced four simultaneous shocks for India: a supply shock, a price shock, a subsidy shock and an import shock. The simple conclusion, according to Damodare, is that urea experienced a nearly 2.5-fold price jump while DAP prices almost doubled. Price volatility, he says, has emerged as the biggest risk to India’s fertiliser security, with DAP proving far more supply-sensitive than urea.

The consequences of these disruptions extend across the entire agricultural economy. Farmers bear the burden through higher fertiliser prices and supply uncertainties that increase the cost of cultivation. The government faces mounting subsidy bills and growing pressure on public finances. Industry, meanwhile, grapples with working capital stress and inventory risks. The result is a cascading increase in costs across the value chain and difficult policy trade-offs for the exchequer.

Importers today face challenges that extend far beyond the price of fertiliser itself. Red Sea disruptions have lengthened transit times and worsened port congestion. Exchange rate volatility has increased the cost of letters of credit and inflated inventory carrying costs. Procurement has become increasingly uncertain, with raw material shortages and unpredictable pricing creating an environment in which, as Damodare puts it, “the cost of uncertainty is becoming as important as the cost of fertiliser itself.”

Simultaneously, climate change is transforming agricultural economics. El Niño events and growing water scarcity are making every drop of water and every unit of nutrient increasingly valuable. Traditional models of indiscriminate fertiliser use are becoming progressively less efficient in a world where resources are constrained and climate variability is intensifying.

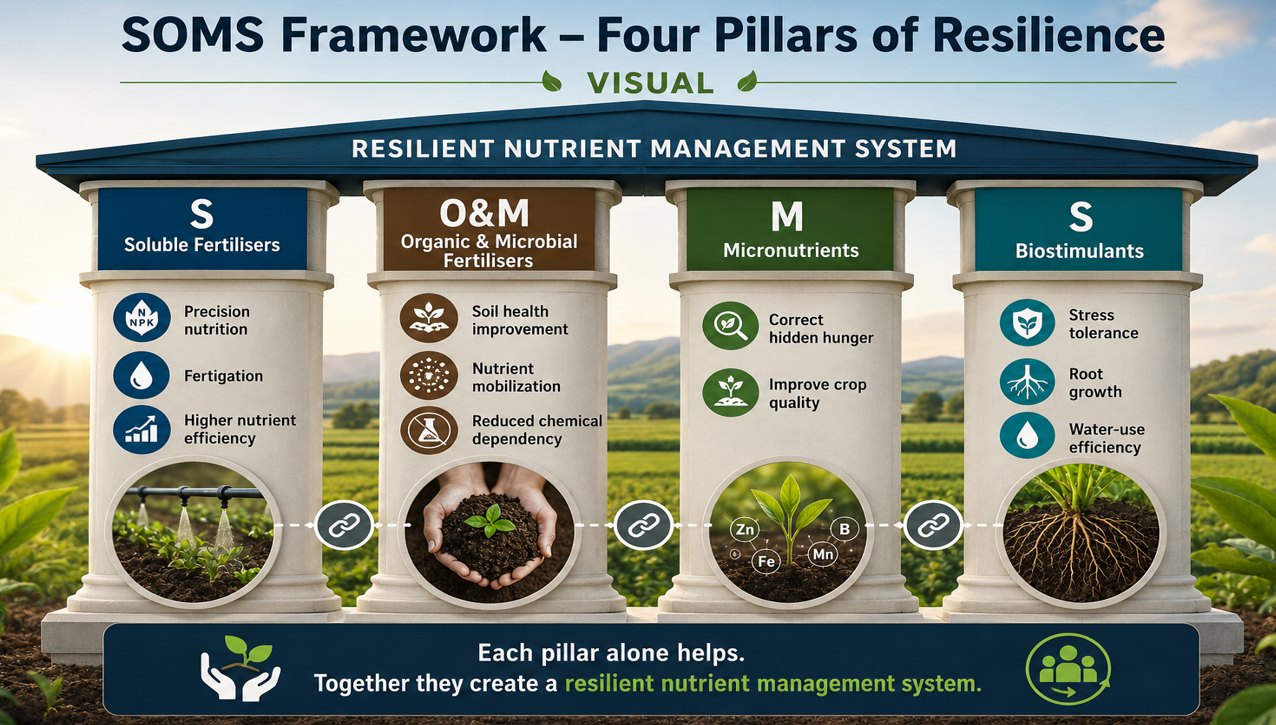

It is in this context that the SOMS framework—Soluble Fertilisers, Organic and Microbial Fertilisers, Micronutrients and Biostimulants—has emerged as a potential model for resilient nutrient management. According to Damodare, SOMS is not merely a collection of products but a framework designed to maximise nutrient-use efficiency and minimise dependence on imported chemical fertilisers.

The first pillar, soluble fertilisers, focuses on precision nutrition and fertigation, enabling higher nutrient-use efficiency. The second pillar, organic and microbial fertilisers, aims to improve soil health, mobilise nutrients and reduce dependence on synthetic inputs. The third pillar, micronutrients, seeks to address hidden hunger in soils and improve crop quality. The fourth pillar, biostimulants, enhances stress tolerance, promotes root growth and improves water-use efficiency. Individually, each pillar contributes to productivity; collectively, they create what proponents describe as a resilient nutrient management system.

The framework becomes particularly relevant during drought years. SOMS is designed to improve water productivity, nutrient productivity and stress tolerance, thereby delivering higher yields under adverse conditions. It seeks to enable farmers to produce more output with less water and fewer inputs while generating more reliable returns.

Perhaps the strongest evidence in favour of the approach comes from field trials conducted at ICAR-NRC Grapes, Pune, during 2024-25. The trials demonstrated that the SOMS treatment used only 207.5 kilograms of chemical fertiliser per acre compared with 554 kilograms under a conventional 75 per cent programme and 770 kilograms under a fully conventional programme. In other words, the SOMS approach required nearly 73 per cent less chemical fertiliser than conventional farming.

Despite the lower fertiliser application, the results were significantly superior. The SOMS treatment recorded yields of 24.25 tonnes per hectare compared with 19.77 tonnes under the conventional 75 per cent programme and 17.59 tonnes under conventional practice. Bunch weight improved to 442.9 grams compared with 401.3 grams and 384.3 grams under conventional systems. Fruit quality, measured through TSS, rose to 24.89 degrees Brix compared with 24.00 and 22.96 degrees respectively. Acidity levels were lower and fruitfulness was higher. Most importantly, the benefit-cost ratio under SOMS stood at 1:6.33, substantially higher than the ratios of 1:4.07 and 1:3.28 under conventional practices.

The message emerging from the trials is profound: less fertiliser can, under appropriate nutrient management, produce higher yields, better quality and greater profitability.

International experience offers further lessons. Brazil faced severe fertiliser supply risks following the Russia-Ukraine conflict. Instead of relying solely on subsidies, it responded by promoting biological inputs and biostimulants, expanding the use of microbial technologies, implementing nutrient stewardship programmes, diversifying import sources and strengthening government-industry collaboration. These measures reduced vulnerability to global shocks while improving soil health, productivity and long-term food security.

For India, the lessons are increasingly clear. The future of agricultural resilience cannot rest solely on ever-rising subsidies and larger quantities of fertiliser. It will require diversification of nutrient sources, improved efficiency, technological innovation and a transition towards more resilient farming systems.

As Damodare argues, the central question confronting Indian agriculture is no longer how much fertiliser can be applied. The more important question is how much productivity can be extracted from every kilogram of nutrient and every drop of water. In an era characterised by wars, climate volatility and fragile global supply chains, resilience itself has become agriculture’s most valuable input. The future of Indian agriculture may therefore depend less on consuming more fertiliser and more on learning to do far more with much less.

— Suchetana Choudhury (suchetana.choudhuri@agrospectrumindia.com)