Friday, 10 July 2026

As China’s buying appetite cools and Europe’s production slows, Rabobank sees the United States and Argentina emerging as the next engines of dairy exports

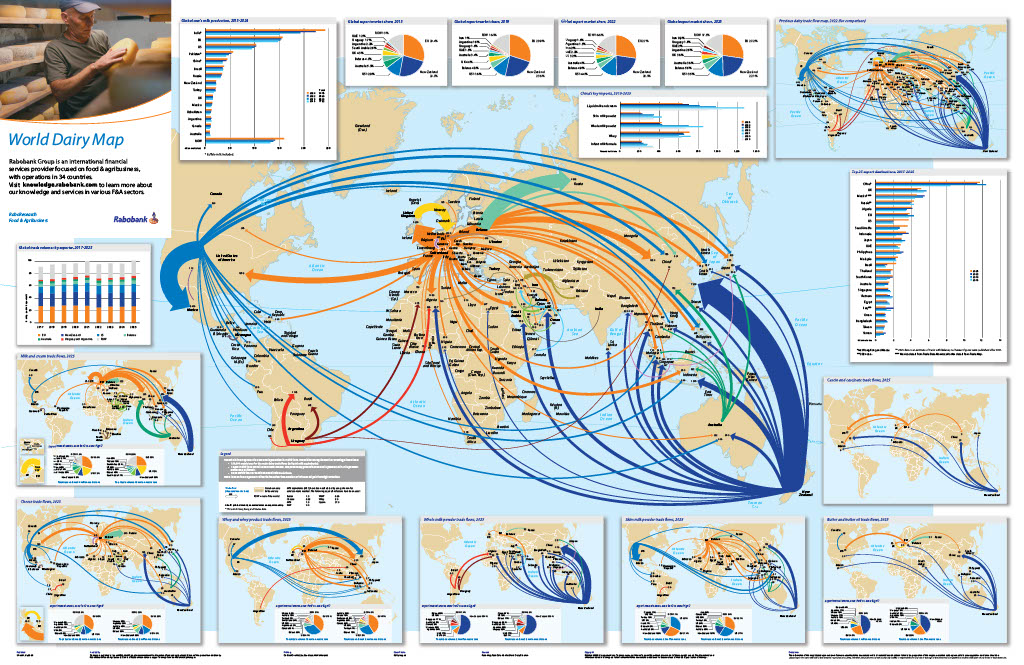

For years, global dairy trade revolved around a familiar equation: Europe supplied, New Zealand dominated exports, and China absorbed an ever-growing share of the world’s milk. That formula is beginning to break down. A new analysis by RaboResearch, the research arm of Rabobank, suggests the dairy industry is entering a structural transition in which demand is spreading beyond China, supply growth is shifting towards the Americas, and cheese—not milk powder—is emerging as the product that will define the next decade of international trade.

The numbers illustrate just how quickly the landscape is changing. Global dairy trade has expanded from 91.1 billion kilograms of liquid milk equivalent in 2017 to more than 101 billion kilograms in 2025. Growth has remained remarkably resilient despite supply disruptions and geopolitical uncertainty, averaging close to two per cent annually. But beneath that steady expansion, the competitive balance is quietly shifting. Europe remains the world’s largest exporter, yet its share of global trade is gradually slipping as the United States, Argentina and Uruguay steadily gain ground.

Perhaps the biggest surprise is not on the supply side, but on the demand side. China is still the world’s largest dairy importer, but it is no longer the growth story exporters once relied upon. As domestic milk production improves and consumption weakens, Chinese purchases of liquid milk and milk powders have fallen sharply from their 2021 peak. Exporters are now looking elsewhere—to the Middle East, Southeast Asia and increasingly Brazil—to drive their next phase of growth. Brazil alone has nearly doubled its dairy imports since 2022, underlining how new consumption centres are beginning to reshape global trade flows.

What stands out most in Rabobank’s analysis is that cheese has moved from being simply another dairy category to becoming the industry’s economic powerhouse. Global cheese trade has expanded by 40 per cent since 2017, outpacing virtually every other dairy product. The reason extends beyond consumer preference. Cheese production also generates whey, an ingredient whose value has surged with the rapid growth of sports nutrition, medical nutrition and high-protein diets linked to GLP-1 weight-loss therapies. For processors, investing in cheese increasingly means capturing value from two fast-growing markets instead of one.

That shift is already influencing investment decisions. While European processors are directing a larger share of available milk towards higher-value cheese production, the United States is investing aggressively in new cheese manufacturing capacity, positioning itself to capture growing global demand. Argentina, meanwhile, is re-emerging as a serious export contender following policy reforms that have revived production, even as Europe faces mounting constraints from environmental regulation, sustainability targets and an ageing farming population.

India, despite its position as the world’s largest milk producer, is notably absent from the export growth story—for now. Rabobank notes that rising domestic consumption continues to absorb most additional milk production, leaving limited volumes available for international markets. While India’s dairy sector continues to expand, its influence remains overwhelmingly domestic rather than export-led. The report ultimately argues that the next chapter of global dairy trade will be shaped less by who produces the most milk and more by who can convert that milk into higher-value products while serving a rapidly changing map of demand. As China’s dominance as the world’s growth engine fades and emerging markets gain prominence, the geography of dairy trade is being redrawn—and the winners are likely to be those investing in value rather than volume.