Friday, 12 June 2026

Wholesale mandi data reveals strengthening paddy prices and improving demand fundamentals, while wheat continues to face downward pressure despite higher MSP support and ongoing procurement efforts.

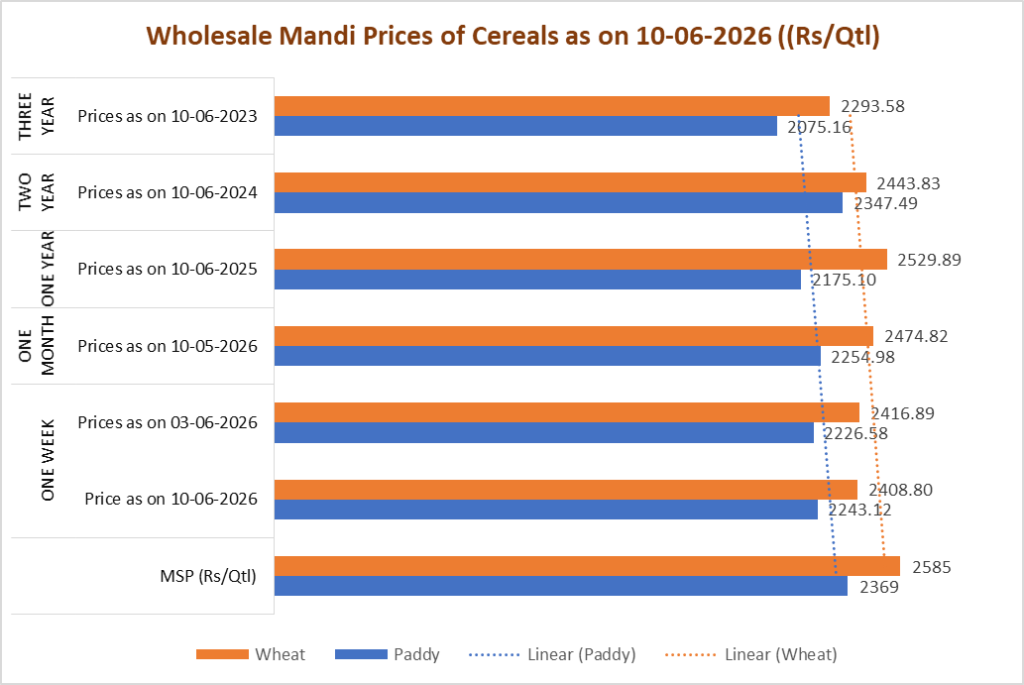

India’s cereal markets presented a mixed picture in early June, with paddy prices registering steady gains across multiple timeframes while wheat continued to trade lower, reflecting divergent supply-demand dynamics in the country’s two most important staple crops.

According to the latest wholesale mandi data released by the Department of Agriculture & Farmers Welfare (DA&FW) through the Agmarknet platform, paddy prices rose to Rs 2,243.12 per quintal as of June 10, 2026, marking a 0.74 per cent increase over the previous week and a 3.12 per cent rise compared to the same period last year. However, paddy remained below its Minimum Support Price (MSP) of Rs 2,369 per quintal, indicating that market prices have yet to fully align with government support levels despite recent improvements.

The positive momentum in paddy markets comes against the backdrop of strong procurement activity, stable domestic demand, and anticipation surrounding the upcoming kharif sowing season. Compared with June 2023, paddy prices have climbed 8.09 per cent, underscoring the crop’s longer-term resilience despite fluctuations witnessed over the past two years. Nevertheless, prices remain 4.44 per cent lower than June 2024 levels, reflecting the impact of ample supplies and periodic market corrections.

In contrast, wheat prices continued to soften. Wholesale mandi prices stood at Rs 2,408.80 per quintal, down 0.33 per cent from a week earlier and 2.66 per cent lower than a month ago. More notably, wheat prices have declined 4.78 per cent year-on-year, suggesting that recent procurement interventions and policy measures have yet to translate into stronger open-market pricing.

The continued weakness in wheat prices is significant given the crop’s MSP of Rs 2,585 per quintal, leaving mandi prices nearly 7 per cent below the government support benchmark. The gap highlights ongoing pressure from adequate domestic availability, substantial government procurement, and efforts to maintain price stability amid concerns over food inflation.

Despite the current softness, wheat has still delivered a 5.02 per cent gain compared with June 2023, indicating that the market remains structurally stronger than it was three years ago. However, compared with June 2024, prices are down 1.43 per cent, reflecting the market’s adjustment to improved supply conditions following successive procurement campaigns.

The contrasting performance of paddy and wheat illustrates the evolving dynamics within India’s cereal economy. While paddy is benefiting from seasonal demand expectations and preparations for the upcoming cultivation cycle, wheat is experiencing the effects of comfortable inventories and active government market management aimed at ensuring food security and price stability.