Wednesday, 10 June 2026

Pressure on fertilizer supplies and elevated energy prices add uncertainty to markets, despite a broadly comfortable global cereal supply situation

World food commodity prices rose in March for the second month in a row, due largely to higher energy prices linked to the conflict escalation in the Near East, according to the latest benchmark measure released Friday by the Food and Agriculture Organization of the United Nations (FAO).

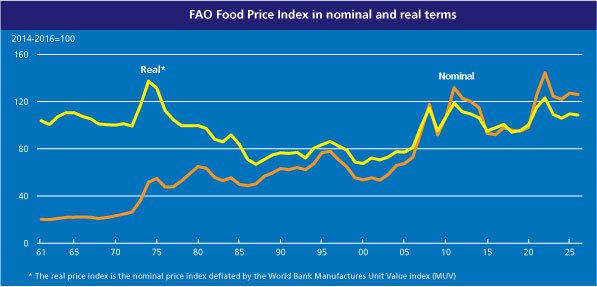

The FAO Food Price Index, which tracks monthly changes in the international prices of a basket of globally-traded food commodities, averaged 128.5 points in March, up 2.4 percent from February and 1.0 percent above its level a year ago.

The FAO Cereal Price Index increased by 1.5 percent from the previous month, driven primarily by higher world wheat prices, which rose 4.3 percent due to drought-related deterioration of crop prospects in the United States of America and expectations of reduced plantings in Australia due to higher fertilizer costs. Global maize quotations edged up slightly, as ample global availability offset concerns over fertilizer affordability and indirect support from greater ethanol demand prospects linked to the rising energy prices. The FAO All-Rice Price Index declined by 3.0 percent in March, driven by harvest timing, weaker import demand, and currency depreciations against the United States dollar.

“Price rises since the conflict began have been modest, driven mainly by higher oil prices and cushioned by ample global cereal supplies,” said FAO Chief Economist Máximo Torero. “But if the conflict stretches beyond 40 days with high input costs with current low margins, farmers will have to choose: farm the same with fewer inputs, plant less, or switch to less intensive fertilizer crops. Those choices will hit future yields and shape our food supply and commodity prices for the rest of this year and all of the next.”

The FAO Vegetable Oil Price Index increased by 5.1 percent from February to stand 13.2 percent higher than its year-earlier level. International quotations for palm, soy, sunflower and rapeseed oil all rose, reflecting spillover effects from the sharp increases in crude oil prices, which catalyzed expectations of stronger demand for biofuels.

The FAO Meat Price Index increased by 1.0 percent from the previous month, driven by a surge in pig meat prices in the European Union ahead of strengthening seasonal demand, along with higher world bovine meat prices, particularly in Brazil, where exportable supplies were curtailed by tightening cattle availability. Ovine and poultry meat prices declined, partly due to logistical constraints limiting access to markets in the Near East.

The FAO Dairy Price Index increased by 1.2 percent, driven primarily by higher quotations for milk powders amid a seasonal decline in supplies in Oceania. International cheese prices declined further in the European Union driven by higher production and weak export demand, while rising in Oceania for the opposite reasons.

The FAO Sugar Price Index increased by 7.2 percent in March. Rising expectations that Brazil, the main sugar exporter, would use more sugarcane to produce ethanol to counter higher international crude oil prices overweighed a generally favourable global supply outlook for the current season, supported by good harvest progress in India and Thailand.

Record wheat plantings in South Asia partly offsets declines elsewhere

FAO also released today updated assessments of global wheat and maize production in 2026, both of which appear on course to drop modestly from high levels, though remaining above their past five-year averages.

With most of the world’s wheat crop already planted, FAO forecasts worldwide harvests of 820 million tonnes, a 1.7 percent drop from the previous year. Lower prices and adverse weather conditions are anticipated to curb wheat output in the European Union, the Russian Federation, and the United States of America, while production in India is expected to hit a record high. Improved rainfall is expected to improve yields and overall outputs in the Islamic Republic of Iran, Türkiye, and across North Africa.

However, the escalation of conflict in the Near East, with associated higher energy and fertilizer prices and disruptions to production and supply chain routes, as well as the prospect of some farmers shifting towards less fertilizer-intensive crops, has introduced additional uncertainty into the outlook for wheat and maize, according to the new Cereal Supply and Demand Brief.

Maize harvesting is already underway south of the equator, and output is expected to be above average in Argentina, Brazil, and South Africa.

FAO has also updated several forecasts, now projecting global cereal production in 2025 at 3 036 million tonnes, 5.8 percent higher than the previous year. World rice output is projected to expand by 2.0 percent, driven by Bangladesh, Brazil, China, India, and Indonesia, to reach a record 563.3 million tonnes.

World cereal utilization in 2025/26 is forecast to rise by 2.4 percent on the year to 2 945 million tonnes, while global cereal stocks will likely expand by 9.2 percent to 951.5 million tonnes. The world cereal stocks-to-use ratio at the end of seasons in 2025/26 is forecast to stand at 32.2 percent, underlining an overall comfortable global supply situation. FAO’s forecast for world trade in cereals in 2025/26 stands at 505.3 million tonnes.