Friday, 3 July 2026

Ample wheat, maize, and rice production lifts world stocks to their highest level in more than two decades

Global cereal markets are entering 2026 on firmer footing, as record harvests and resilient production across major exporters fuel a broad-based recovery in world grain stocks, according to FAO’s latest assessment.

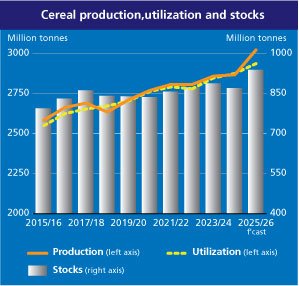

FAO now forecasts global cereal production in 2025 to reach 3.023 billion tonnes, up 0.7 percent from last month and marking a new all-time high. Stronger-than-expected wheat yields in Argentina, Canada, and the European Union underpin the upward revision, pushing global wheat output to a record level. Coarse grain production has also been revised higher, driven by expanded maize acreage and improved yields in China and the United States, alongside stronger barley outputs in Australia and Canada.

Rice production is likewise set to reach new highs. FAO has raised its 2025/26 global rice forecast to 561.6 million tonnes (milled basis), a 2.0 percent year-on-year increase, led primarily by India, supported by strong Rabi plantings and higher official harvest estimates. Additional gains in Bangladesh, Brazil, China, and Indonesia more than offset weather-related setbacks in parts of Southeast Asia and revisions in Venezuela.

Early Signals for 2026 Crops

Looking ahead, early indicators for the 2026 wheat crop suggest generally favourable prospects across much of the northern hemisphere. In the European Union and the United Kingdom, slightly higher plantings and supportive weather conditions point to yields above the five-year average, though below last year’s exceptional results. India is expected to plant a record wheat area amid strong domestic prices and favourable growing conditions, while yield prospects in the Russian Federation and parts of the United States remain under pressure from moisture deficits and weather volatility.

In the southern hemisphere, early expectations for 2026 coarse grains are broadly positive. Argentina and Brazil are projected to expand maize production on the back of improved planting incentives and strong demand, while South Africa is forecast to increase maize area by 3 percent year-on-year, supported by favourable rainfall outlooks.

Utilization and Trade Continue to Expand

Global cereal utilization in 2025/26 is forecast at 2.938 billion tonnes, up 2.2 percent year-on-year, driven mainly by higher maize use for feed and industrial purposes. Demand growth is particularly notable in Egypt, reflecting rapid expansion in poultry and livestock production, and in the United States, where maize use for ethanol has strengthened.

World cereal trade is projected to rise to 501.0 million tonnes in 2025/26, a 3.6 percent increase from the previous season. Wheat trade is forecast to rebound, with exporters such as Argentina, Australia, the European Union, and the Russian Federation regaining market share, while coarse grain trade growth is supported by increased maize imports by China, Egypt, and the Islamic Republic of Iran.

Stocks Reach a 25-Year High

With production outpacing utilization, FAO now expects world cereal stocks to rise by 67.6 million tonnes by the close of the 2026 seasons, lifting the global stocks-to-use ratio to 31.8 percent, its highest level since 2001. Maize inventories account for the largest increase, led by Brazil and the United States, while wheat and rice reserves are also set to expand notably, including significant stock accumulation in China and India.

Together, these developments signal a period of improved supply resilience for global cereal markets—providing a buffer against climate volatility, geopolitical disruptions, and rising demand heading into the latter half of the decade.

To read more, click: https://www.fao.org/worldfoodsituation/csdb/en/