Wednesday, 3 June 2026

While soybean holds marginally above support levels, groundnut, sesamum and sunflower trade below MSP, highlighting widening gaps between policy benchmarks and market prices in India’s oilseed economy

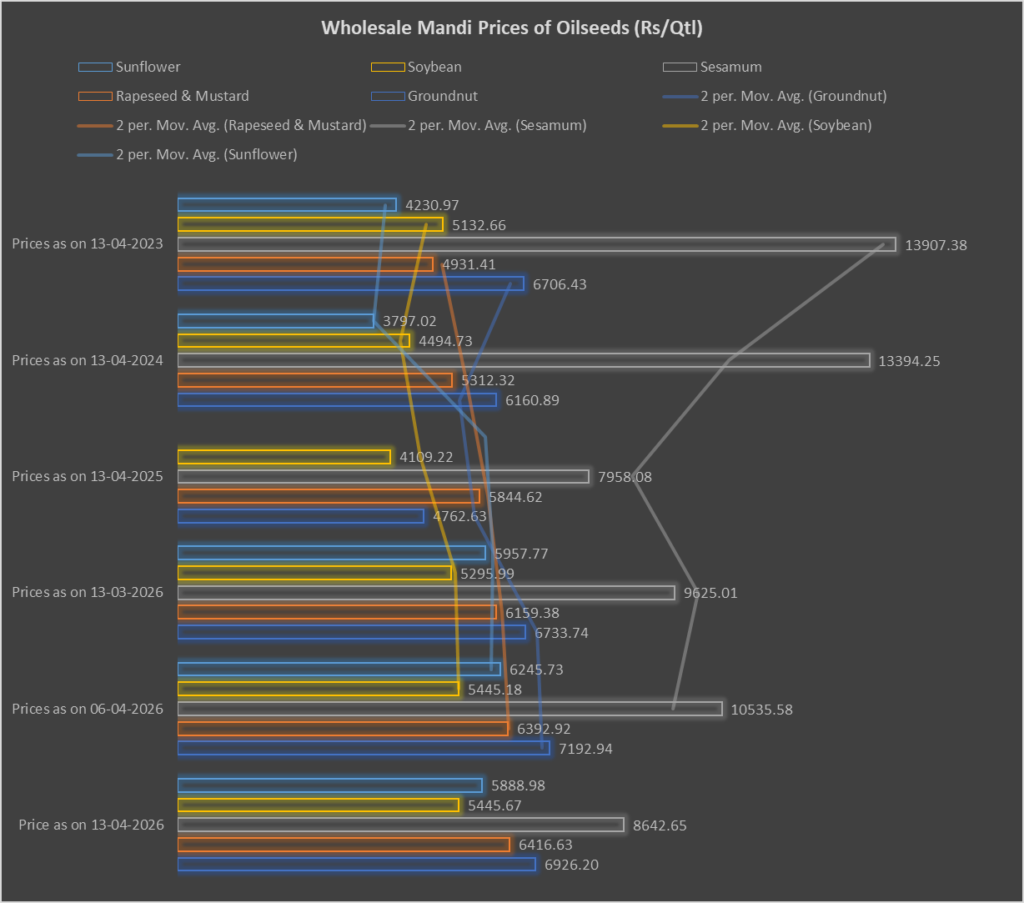

India’s wholesale oilseed markets are exhibiting increasingly divergent trends, with strong long-term price gains across key commodities now tempered by short-term corrections and uneven alignment with Minimum Support Prices (MSPs), according to the latest Agmarknet mandi data.

Groundnut prices stood at Rs 6,926.20 per quintal as of April 13, 2026, remaining below the MSP of Rs 7,263. The commodity has delivered a robust annual increase of 45.42 per cent from Rs 4,762.63 a year ago, alongside gains of 12.42 per cent over two years and 3.27 per cent over three years. However, this strong performance has been accompanied by recent weakness, with prices declining 3.70 per cent over the past week from Rs 7,192.94, even as they rose 2.85 per cent over the past month from Rs 6,733.74. This pattern suggests that while groundnut remains a strong long-term performer, it is currently experiencing short-term price correction, potentially reflecting demand moderation or market consolidation.

Rapeseed and mustard present a contrasting picture, emerging as the most stable oilseed in the current cycle. Prices reached Rs 6,416.63 per quintal, comfortably above the MSP of Rs 6,075, indicating sustained market strength. The commodity recorded marginal weekly growth of 0.37 per cent from Rs 6,392.92 and a stronger monthly increase of 4.17 per cent from Rs 6,159.38. Over longer horizons, rapeseed and mustard prices have risen 9.78 per cent year-on-year from Rs 5,844.62, 20.78 per cent over two years from Rs 5,312.32, and 30.11 per cent over three years from Rs 4,931.41. This steady upward trajectory across all timeframes highlights a balanced demand-supply dynamic and positions rapeseed and mustard as the most structurally stable oilseed in the market.

Sesamum, by contrast, reflects significant volatility and long-term weakness. Prices fell sharply to Rs 8,642.65 per quintal, well below the MSP of Rs 9,846, marking a steep weekly decline of 17.96 per cent from Rs 10,535.58 and a monthly drop of 10.20 per cent from Rs 9,625.01. Although prices remain 8.60 per cent higher than a year ago at Rs 7,958.08, the longer-term trend is markedly negative, with declines of 35.47 per cent from Rs 13,394.25 over two years and 37.85 per cent from Rs 13,907.38 over three years. This sustained erosion underscores structural challenges in the sesamum market, where short-term fluctuations are overshadowed by a persistent downward trajectory.

Soybean prices stood at Rs 5,445.67 per quintal, marginally above the MSP of Rs 5,328, reflecting relative stability. Prices remained flat on a weekly basis at 0.00 per cent compared to Rs 5,445.18, while registering a 2.82 per cent monthly increase from Rs 5,295.99. On a longer-term basis, soybean has shown consistent strength, with a 32.52 per cent increase over the past year from Rs 4,109.22, a 21.15 per cent rise over two years from Rs 4,494.73, and a 6.09 per cent gain over three years from Rs 5,132.66. This combination of short-term stability and sustained medium-term growth positions soybean as one of the more balanced performers in the oilseed segment.

Sunflower prices were recorded at Rs 5,888.98 per quintal, significantly below the MSP of Rs 7,721, highlighting a notable gap between market realization and support levels. Prices declined 5.71 per cent over the past week from Rs 6,245.73 and 1.15 per cent over the past month from Rs 5,957.77. While year-on-year comparison is not available, sunflower has demonstrated exceptional growth over longer periods, rising 55.09 per cent from Rs 3,797.02 over two years and 39.18 per cent from Rs 4,230.97 over three years. Despite these strong historical gains, the recent downward trend indicates short-term softness, suggesting that the commodity may be undergoing a cyclical correction after a period of rapid appreciation.

Taken together, the data points to a clear shift in India’s oilseed market dynamics. While long-term price trends remain broadly positive across most commodities, short-term movements are increasingly mixed, with declines observed in groundnut, sesamum, and sunflower, and relative stability in soybean and rapeseed and mustard. The divergence is further underscored by MSP alignment, with only rapeseed and mustard and soybean trading above their support prices, while groundnut, sesamum, and sunflower remain below MSP levels.

The broader implication is that India’s oilseed markets are no longer moving in a synchronized cycle but are instead driven by commodity-specific fundamentals. Strong multi-year gains in crops such as sunflower and groundnut coexist with structural declines in sesamum and steady growth in rapeseed and mustard, reflecting variations in demand, supply conditions, and market sentiment.

In this evolving landscape, price discovery is increasingly being shaped by market forces rather than policy benchmarks, with MSP acting as a reference rather than a binding floor for most commodities. As a result, stakeholders across the agricultural value chain are likely to face a more complex operating environment, where navigating commodity-specific trends will be critical to managing risk and capturing value.