Sunday, 21 June 2026

Deepak Fertilisers and Petrochemicals Corporation Ltd. (DFPCL), one of India’s largest producers of industrial chemicals and fertilisers, announced robust results for Q1 FY26, underlining the company’s steady transition towards specialty and value-added segments across its core businesses. A 17 per cent YoY surge in consolidated operating revenue and a 22 per cent jump in net profit mark a resilient start to FY26, despite a challenging global commodities backdrop.

“The strong start to FY26 underscores the impact of our strategic transformation and disciplined execution,” stated S.C. Mehta, Chairman & Managing Director of DFPCL. “Our continued focus on specialty products, customer engagement, and operational agility is driving tangible results.”

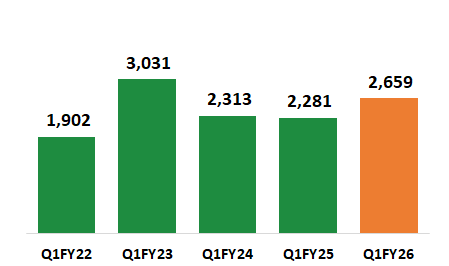

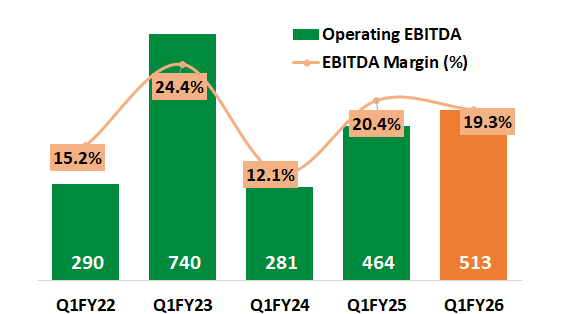

In the first quarter of FY26, Deepak Fertilisers reported consolidated operating revenue of Rs 2,659 crore, marking a 17 per cent year-on-year increase compared to Rs 2,281 crore in Q1 FY25. Revenue remained flat on a sequential basis from Rs 2,667 crore in Q4 FY25. Operating EBITDA stood at Rs 513 crore, up 10 per cent from Rs 464 crore in the same quarter last year and a 7 per cent increase over Rs 480 crore in the previous quarter. However, EBITDA margins narrowed to 19.3 per cent from 20.4 per cent in Q1 FY25, a decline of 106 basis points, though they improved by 130 basis points sequentially.

Profit Before Tax (PBT) rose to Rs 345 crore, reflecting a 28 per cent YoY increase and 8 per cent growth over Q4. Net Profit After Tax (PAT) reached Rs 244 crore, up 22 per cent from Rs 200 crore last year. On a quarter-over-quarter basis, PAT declined 12 per cent from Rs 278 crore in Q4 FY25, which had included a one-time deferred tax reversal of Rs 37 crore. PAT margins improved by 38 basis points YoY to 9.1 per cent, although they dipped 114 basis points sequentially from 10.2 per cent.

Strategic and Operational Milestones

In its Crop Nutrition Business, the company saw standout performance in Q1. Croptek volumes surged 73 per cent year-on-year and grew 10 per cent over the previous quarter, reflecting strong market acceptance of its precision crop nutrition strategy. Specialty fertilisers—such as Bensulf Superfast, Solutek, and WSF NPKs—also performed well, growing 21 per cent YoY and nearly doubling sequentially.

DFPCL’s field engagement strategy continues to yield strong returns: the company conducted 3,558 grassroots outreach activities including crop seminars, demonstrations, farmer group meetings, and field visits, directly engaging nearly 1.77 lakh farmers. With a normal monsoon forecast for June–September 2025 by Skymet, the company anticipates robust Kharif demand across key crops such as sugarcane, soybean, cotton, arecanut, and corn. This, combined with strong brand recall for Mahadhan products and a sharp farmer-focused marketing strategy, is expected to drive growth in the coming quarters.

The Mining Chemicals segment maintained full capacity utilisation for its Technical Ammonium Nitrate (TAN) production during the quarter. TAN sales volumes increased by 7 per cent year-on-year and remained stable sequentially. The company’s consumer-centric strategy in the mining segment is also bearing fruit, with the B2C channel now contributing 16 per cent of segment revenue. While export volumes were temporarily lower in Q1 due to quota constraints, a favourable regulatory development in June 2025 raised the TAN export quota to 50,000 MT annually, setting the stage for improved export performance going forward. Although early monsoons impacted LDAN consumption, coal production remained steady, while steel and cement output showed moderate growth of 1–3 per cent.

In the Industrial Chemicals business, DFPCL demonstrated resilience amid subdued market conditions. Isopropyl Alcohol (IPA) volumes rose by 27 per cent YoY and a significant 51 per cent QoQ, largely due to a low base effect and successful plant modifications completed in Q4. Nitric Acid volumes also showed robust performance, growing 15 per cent YoY and 3 per cent QoQ.

The company continued to focus on high-value applications and introduced 11 new products under the “PuroGuard+” specialty brand in Q1 to meet targeted customer needs. Notably, PICKBRITE—a specialty product for stainless steel pickling—showed encouraging results in customer trials, and DFPCL secured approvals from large domestic players for its solar-grade nitric acid. Despite softness in acetone prices and elevated inventories impacting IPA sentiment, and seasonal monsoon effects affecting downstream TAN demand, the company maintained its momentum by intensifying customer segmentation and innovation-led targeting strategies.

Legal and Financial Clarity: ITAT Ruling Favourable

DFPCL’s subsidiary, Mahadhan AgriTech Ltd. (MAL), received a favourable ruling from the Income Tax Appellate Tribunal (ITAT), Mumbai, for assessment years 2016–17 to 2020–21. The ITAT nullified tax demands aggregating Rs 581 crore by deleting all previous additions made by the Income Tax Department. As a consequence of this ruling, penalty orders totaling Rs 479 crore for assessment years 2015–16 to 2018–19 are also expected to be withdrawn. This outcome reinforces the company’s strong legal compliance framework and brings financial clarity going forward.

“This ruling reaffirms our robust compliance systems and legal interpretations,” said the CMD. “It provides financial clarity and strengthens confidence in our governance architecture.”

Capex and Debt Update: Building the Foundation for FY27

During Q1 FY26, DFPCL invested Rs 377 crore towards ongoing capital expenditure projects. Despite this, the company successfully reduced net debt from Rs 3,305 crore at the end of March 2025 to Rs 3,078 crore by June 2025. Net debt-to-EBITDA improved from 1.72x to 1.50x, reflecting both operational efficiency and financial prudence.

The company’s two major capex projects— the Gopalpur TAN plant and the Dahej Nitric Acid complex—are progressing as planned. The Gopalpur project is approximately 80 per cent complete with a total capex outlay of Rs 2,675 crore, while the Dahej project is 57 per cent complete at Rs 1,983 crore. Both facilities are on track for commissioning by the end of FY26. All major statutory approvals have been obtained, and critical equipment has been ordered, with deliveries in progress. Both plants are strategically located to mitigate raw material supply risks and ensure secure offtake.

Outlook: Eyes on Kharif and Export Markets

With favourable monsoon projections, a strong uptick in farmer engagement, and increasing traction in the specialty portfolio, DFPCL expects to sustain its growth momentum through the Kharif season and beyond. The expanded export quota for TAN, improved capacity utilization, and differentiated industrial product portfolio are set to further strengthen performance in H2. The company remains focused on building sustainable value through sharper execution, deeper customer engagement, and long-term innovation.

“We remain committed to delivering sustainable value, backed by sharper execution, deeper customer engagement, and a clear focus on long-term value creation,” Mehta concluded.